Crude oil prices react to many types of geopolitical events, from weather disasters to wars, revolutions and economic growth or recessions. |

50 years of ups and downs

Global oil production began in the mid-1800s and grew rapidly in the first half of the 20th century. For much of that time, oil majors companies like Chevron, Amoco and Mobil that were created after the Supreme Court ordered the breakup of Standard Oil in 1911 operated effectively as a cartel, maintaining production at levels that kept oil abundant and cheap to encourage its consumption.

This ended when Iran, Iraq, Kuwait, Saudi Arabia and Venezuela formed the Organization of Petroleum Exporting Countries in 1960, nationalizing their oil reserves and gaining real supply power. Over the following decades, other nations in the Middle East, Asia, Africa and Latin America joined some temporarily, others permanently.

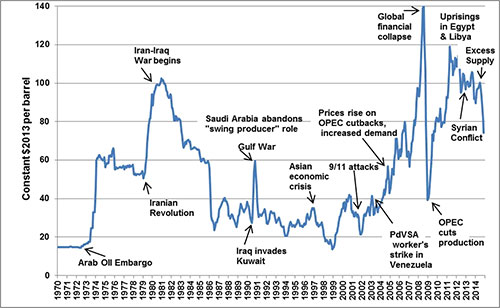

In 1973, Arab members of OPEC cut their oil production when Western countries supported Israel in the Yom Kippur War with Egypt and Syria. World oil prices shot up fourfold, from an average of $2.90 per barrel to $11.65.

In response, government leaders in wealthy countries introduced policies to stabilize oil supplies. These included finding more oil, investing in energy research and development, and creating strategic oil reserves that governments could use to mitigate future price shocks.

But six years later, oil prices more than doubled again when Irans revolution halted that countrys output. Between mid-1979 and mid-1980, oil rose from $13 per barrel to $34. Over the next several years, a combination of economic recession, replacing oil with natural gas for heating and industry, and shifting to smaller vehicles helped to mitigate oil demand and prices.

The next major shock came in 1990 when Iraq invaded Kuwait. The United Nations imposed an embargo on trade with Iraq and Kuwait, which raised oil prices from $15 per barrel in July 1990 to $42 in October. U.S. and coalition troops moved into Kuwait and defeated the Iraqi army in just a few months. During the campaign, Saudi Arabia increased oil production by more than 3 million barrels per day, roughly the amount previously supplied by Iraq, to help dampen the increase and shorten the period of higher prices.

More disruptive price shocks occurred in 2005-2008 and 2010-2014. The first resulted from increased demand generated by economic growth in China and India. At that time, OPEC was unable to expand production due to long-term lack of investment.

The second shock reflected the impacts of Arab Spring pro-democracy protests in the Middle East and North Africa, combined with conflict in Iraq and international sanctions that Western nations placed on Iran to slow its nuclear weapons program. Together, these events pushed oil prices above $100 per barrel for a four-year stretch the longest such period on record. Relief finally came via a flood of new oil from shale production in the U.S..

A pefect storm in 2022Today, multiple factors are raising oil prices. There are three key elements:

Oil demand has grown more rapidly than expected in recent months as countries emerged from pandemic lockdowns.

OPEC+, a loose partnership between OPEC and Russia, has not raised production at a commensurate level, and neither have U.S. shale oil companies.

Countries have drawn on stocks of oil and fuel to fill the supply gap, reducing this emergency cushion to low levels.

These developments have made oil traders worry about looming scarcity. In response, they have bid oil prices up. Its worth noting that while consumers often blame oil companies (and politicians) for high oil prices, these prices are set by commodity traders in venues such as the New York, London and Singapore stock exchanges.

Against this backdrop, Russia attacked Ukraine on Feb. 24, 2022. Traders saw the potential for sanctions on Russian oil and gas exports and bid energy prices even higher.

Unexpected factors also have emerged. Major oil companies including Shell, BP and ExxonMobil are ending their operations in Russia. Spot market buyers have rejected seaborne Russian crude, probably for fear of sanctions.

And on March 8, the U.S. and U.K. governments announced bans on imports of Russian oil. Neither country is a major Russian buyer, but their actions set a precedent that some analysts and traders fear could lead to escalation, with Russia reducing or eliminating exports to U.S. allies.

In my view, this set of conditions is unprecedented. It reflects not just increased complexity in the global market, but also an imperative for energy firms which already are under pressure from shareholder climate activists to avoid further reputational damage and leave one of the most oil-rich countries in the world. Some companies, such as BP, are abandoning assets worth tens of billions of dollars.What could ease this shock?

As I see it, the key players that can help curtail this price shock are OPEC mainly, Saudi Arabia and the U.S. For these entities, holding back oil supply is a choice. However, theres no evidence yet that they are likely to change their positions.

Restoring the Iran nuclear deal and lifting sanctions on Iranian oil would add oil to the market, though not enough to greatly reduce prices. More output from smaller producers, such as Guyana, Norway, Brazil and Venezuela, would also help. But even combined, these countries cant match what the Saudis or the U.S. could do to increase supply.

All of these uncertainties make history only a partial guide to this oil shock. Currently there is no way to know how long the factors driving it will last, or whether prices will go higher. This isnt much comfort to consumers facing higher fuel costs around the world.

Scott L. Montgomery, Lecturer, Jackson School of International Studies, University of Washington This article is republished from The Conversation |

Representations of fact and opinions in comments posted are solely those of the individual posters and do not represent the opinions of Sitnews.

Send a letter to the editor@sitnews.us

SitNews ©2022

Stories In The News

Ketchikan, Alaska

Articles & photographs that appear in SitNews are considered protected by copyright and may not be reprinted without written permission from and payment of any required fees to the proper freelance writers and subscription services.

E-mail your news & photos to editor@sitnews.us

Photographers choosing to submit photographs for publication to SitNews are in doing so granting their permission for publication and for archiving. SitNews does not sell photographs. All requests for purchasing a photograph will be emailed to the photographer.